In our first Mates Rates Capital Research Snippets on Next Era Energy (NYSE:NEE), we promised we’d take a look at another stock with a much smaller market cap, called Flux Power Holdings (FLUX).

Well that day has finally arrived. It’s taken a bit longer to get there than we initially planned, but we’ve now had the chance to digest all the research we’ve done on Flux Power (FLUX), which we’re excited to share with you in our second edition of the Mates Rates Capital Research Snippets.

Quick summary

Flux Power Holdings Inc (FLUX) designs, develops, manufactures and sells rechargeable lithium ion batteries for airport ground support equipment (GSE), forklifts, solar energy storage and other commercial applications.

Another core focus of FLUXs business is developing and distributing battery management system (BMS) software, which serves as the brain of the battery pack, managing cell balancing, charging, discharging, and providing remote based real time battery performance monitoring.

Flux generates revenue by selling products through a distribution network of equipment dealers, OEMs and battery distributors primarily in North America. Their customers range from small companies to Fortune 500 companies.

With a 52-week price range of between $1.89 and $5.45 per share, FLUX can be classified as a penny stock, which are typically highly speculative company stocks that trade for less than $5 per share, according to Investopedia.

You may recognize the term “penny stocks” from The Wolf of Wall Street, which were used by Jordan Belfort to scam investors out of large sums of money. But don’t let this put you off reading up on Flux Power – while low market cap stocks inherently carry more risk, there’s sometimes a chance you’ll find a diamond in the rough.

Pros

- Consistent revenue growth and reduction in losses per share over the past 4 years.

- Increasing net margins, from -169% to -25% over the past 4 years.

Cons

- Currently unprofitable. Reliant on external capital.

- Susceptible to risks such as supply chain issues (increased shipping and material costs, risk of tariffs being implemented by US government on goods imported from China)

- Revenue generation is reliant on a small number of customers. 69% revenue derived from four customers.

How does Flux Power make money?

Flux Power’s primary focus so far has been the material handling sector, which is believed to be a multi billion dollar addressable market. Flux Power has achieved success in this sector through their two business segments; 1) producing rechargeable lithium battery packs, and 2) developing battery management system software.

Rechargeable lithium batteries developed by Flux Power have a range of advantages over existing lead acid batteries and propane based solutions, such as environmental benefits, faster charge times, greater cycle life, and longer run times.

Flux Power’s proprietary battery management system software aims to deliver further operational and financial benefits for customers, primarily by providing access to real-time battery monitoring data that can be used to improve battery performance. Additionally, Flux has designed their battery management system to be compatible with a variety of lithium battery cells, rather than being exclusively compatible with Flux battery packs, which is suspected to help drive uptake of the BMS software in areas of the battery market that may already have been cornered by Flux Power’s competitors.

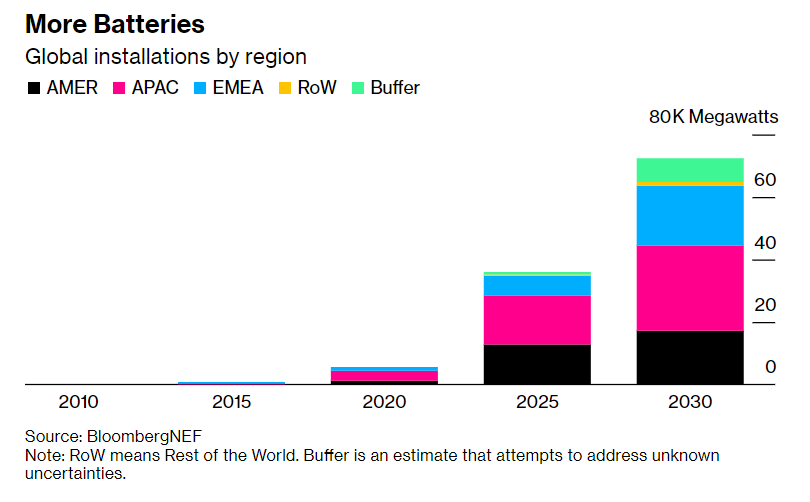

On top of this, further expansion in the stationary energy storage market is expected to provide Flux Power with ongoing opportunities for growth. BloombergNEF expects the capacity of storage systems to grow 15-fold by 2030, largely due to the key role battery storage is expected to play within enabling increasing global adoption of renewable energy solutions, such as wind and solar.

Profitability

Flux Power is currently an unprofitable company, having made a loss of $15.6 M in FY2022. This being said, Flux Power’s revenue is up 84% year on year in 2022, and their revenue has been consistently increasing over the past 4 years.

The reason that Flux power is not yet profiting off this revenue is because their expenses exceed their income, as reflected by their net profit margin of -25.26% in 2022, essentially meaning that it costs Flux Power approximately $1.25 to generate $1 worth of revenue by selling products to their customers.

At the end of the day you can’t sustain running a business over the long term if you’re selling your products for less than what it costs you to make them. To start turning a profit on their revenue, Flux Power is striving to increase their net profit margins, primarily by focusing on reducing costs.

Flux Power plans to reduce costs through a number of approaches such as, utilizing lower cost suppliers, seeking more competitively priced shipping providers, implementing lean manufacturing processes and more.

This cost cutting approach seems to be working quite nicely for Flux Power, as their net profit margins have been trending in the right direction over the past 4 years, going from -169% in 2018 to -25% in 2022.

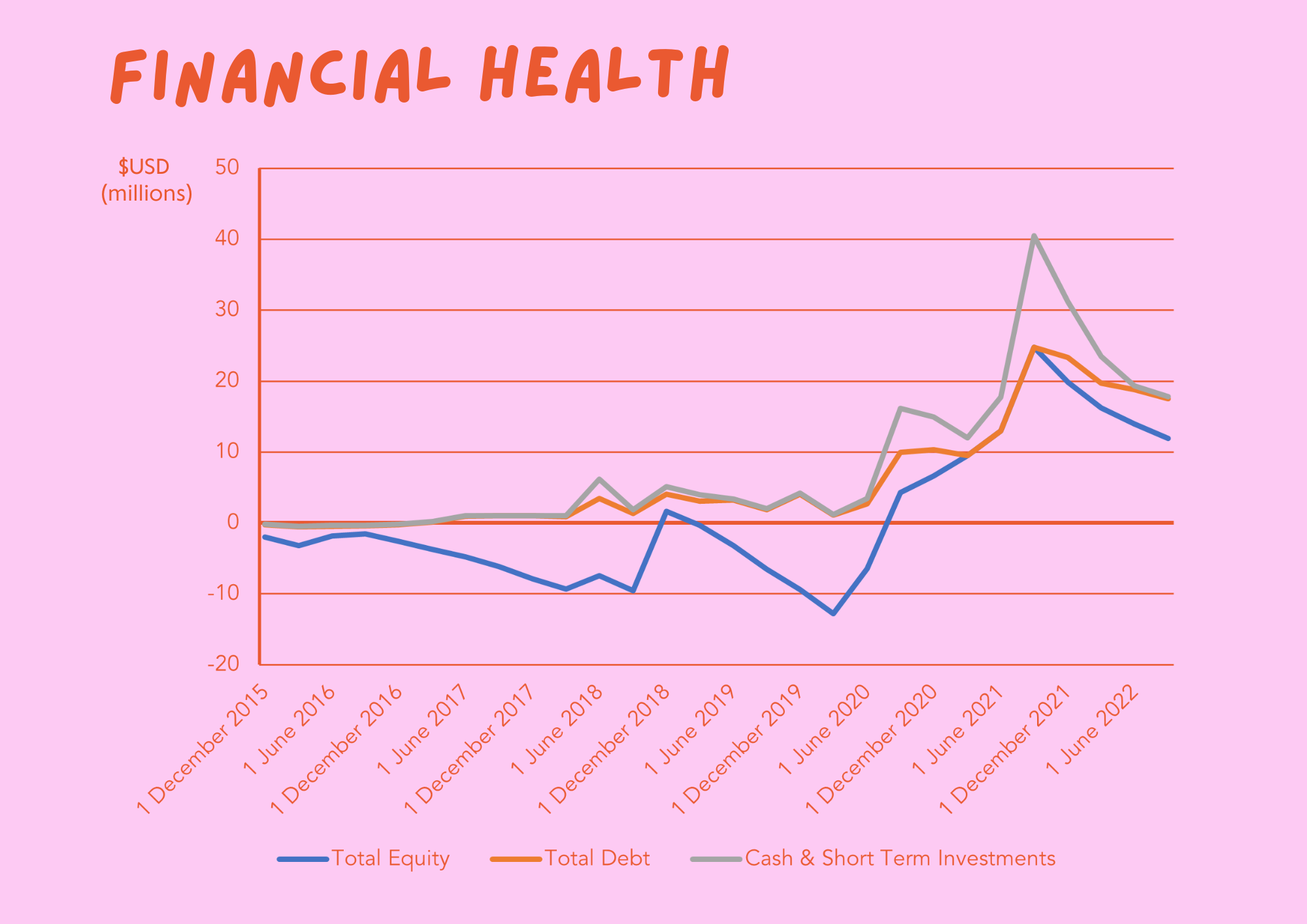

Financial health

A potential cause for concern with Flux Power is that they appear to have a relatively small cash runway, with only $485k free cash available at the end of 2022. To put this into perspective, Flux Power’s net loss from 2022 amounted to $15.6 M, meaning the $485k of free cash that Flux Power had available at the end of 2022 would only be enough to cover about 3% of their current operating expenses.

This being said, it appears that Flux Power has already addressed these concerns regarding cash reserves. Based on their 2022 financial report, Flux has already secured access to capital through the following avenues:

- Forecasted gross margins – value not specified.

- Silicon Valley Bank (SVB) Credit facility – $3.1 M

- Subordinated line of credit (LOC) – $4 M

- Net proceeds of approx. $14M from a registered direct offering of stocks and warrants in Sept 2021.

According to Flux Power management, this capital should be sufficient to fund operations for the next 12 months through 2023.

Flux Power has achieved positive equity since FY2021, which means that their assets are currently worth more than their liabilities. This is primarily because Flux Power has raised a lot of capital through selling shares, rather than issuing debt based products that need to be paid back, such as corporate bonds or bank loans. Issuing shares to investors in return for capital helps to keep debt off the balance sheet, while also allowing Flux to grow their assets.

However in FY2022, Flux Power has added $5.5M of debt to their balance sheet through the Silicon Valley Bank (SVB) credit facility and the subordinate (LOC). To maintain attractiveness from a financial health standpoint, Flux Power will need to continue increasing equity, which could be achieved by successfully increasing their net margins or by issuing more stocks to raise capital.

Risks

Flux Power faces a number of risks as they navigate their journey towards profitability, such as:

Liquidity and capital resources

Currently, Flux Power is running at a loss, which means they are reliant on external investment to fund their business. Therefore, while Flux Power remains an unprofitable company, any events that may prevent Flux from raising capital or securing debt are likely to have measurable impacts on Flux’s ability to continue operations in the future, which could have major impacts on the company share price.

This can make smaller businesses such as Flux Power particular susceptible to prolonged economic downturns, especially when borrowing money is expensive due to high interest rates. Continuing to raise capital by issuing new shares can also be a double edge sword, as it leads to dilution of share prices.

Supply chain risks

The battery cell is an integral component within Flux Power’s battery packs. Rather than manufacturing the battery cells themselves, Flux Power source battery cells from a limited number of manufacturers located in China.

This presents a number of risks that may negatively impact Flux Power’s business, such as increased costs (i.e. fluctuations in materials and shipping prices, implementation of tariffs by the US government on goods imported from China) or even inability to procure components that meet required quality standards, together which could reduce margins for Flux Power and impede progress towards profitability.

Customer attrition

Flux Power currently has a large degree of customer concentration, in which just four major customers together represented approximately $29.3M USD, or 69% or their total revenue in 2022. By having a lot of eggs in one basket, Flux Power risks significant revenue erosion if they were to lose one of these customers, which would likely have a large knock-on effect for Flux Power’s share price.

Conclusion

As a small market cap company that is currently unprofitable, Flux Power’s ability to protect themselves against risks could be their make or break point. Basically, if you don’t have profits flowing in to protect you during economic downturns, it doesn’t take much to destabilize your business, which is why small market cap stocks often inherently carry a lot of risk.

This being said, Flux Power’s fundamentals appear to be trending in the right direction, plus we expect there to be plenty of room for growth in the solar energy storage space.

By developing rechargeable lithium battery packs and software used by lift trucks in the materials handling sector, Flux Power has successfully achieved consistent growth in revenue over the past 4 years.

While Flux Power is an unprofitable company, they’ve been successful at consistently reducing losses per share from -$2.75 to -$0.85 over the past 4 years. During this period, Flux Power has gradually been increasing their net margins from -169% to -25%.

Despite finishing the fiscal year 2022 with a very small cash runway, Flux Power has since successfully raised capital and secured debt, amounting to approx. $21M USD, which their management team believe will be sufficient to fund operations during 2023.

Reducing costs continues to be a big focus for Flux Power’s management in order to further boost their margins, so we’ll continue to keep a close eye on Flux Power’s earnings per share and net margins.

For the purpose of full disclosure, we already hold shares in flux power, having brought at an entry price of 3.02, which are currently up 75% at time of writing.

Overall, Flux’s stock price has seen a lot of volatility, with a beta of 1.18 (above 1 means that Flux is more volatile than the overall market), so we very much expect to see continued price swings – but we’re in it for the long haul, so day to day price movement isn’t something we pay a heap of attention to. With this in mind, please do not use this to guide any of your own investment decisions and remember to always do your own research.

Things to watch with Flux Power (FLUX) moving forward:

- Earnings/losses per share (EPS). Want to see a continued reduction in losses per share. Currently 69% of FLUX Power’s revenue is from four customers, which presents a risk to Flux Power’s EPS, so we’ll also be keeping a lookout for new contracts and customers signings

- Net margins. Want to see a continued increase in net margins. Flux currently spending $1.25 to generate $1 worth of revenue.

And one more thing to keep an eye on:

- Trading activity around key stock price values ($6-12 per share). Many investors who bought shares in Flux Power during 2021 are currently down on their investments. This could influence trading activity if investors are seeking to recoup these losses by selling their holdings when the stock price trends towards their initial buy in price.

Two notable recent capital raises are listed below:

- From Dec 21 2020 through June 30, 2022 Flux Power sold 1,169,564 shares of common stock at an average price of $12.24 per share in an At-The-Market (ATM) offering

- On September 27, 2021, Flux Power sold stocks and warrants to purchase up to an aggregate of 1,071,430 shares of common stock at an offering price of $7.00 per share through a registered direct offering) News on contracts and customer signings. We’d also like to see less customer concentration.

About us

Here at Mates Rates Capital, we’re just a group of mates trying our hand at investing by pooling together a small amount of our hard earned wages each week.

We started Mates Rates Capital as a project to share our tips, tricks, mistakes, and learnings so that you can go start a group investment fund and reap the rewards of investing with friends.

Come along for the ride! 🤙

Legal stuff

The content shared in this article is based on the opinions of Mates Rates Capital and is not financial advice. Any information shared is only current at the time of writing and is provided without consideration of the financial situation of any individual person. Always do your own research. You should consider seeking legal, financial, taxation or other advice before making any investment decisions.