Quick summary

Xero Limited (ASX:XRO) offers a cloud-based accounting software that is designed to help small businesses manage their financials efficiently. Xero is a New Zealand company with offices in Australia, United Kingdom and the United states, growing from humble beginnings in Wellington to becoming one of the largest technology companies on the Australian Stock Exchange (ASX) with a market cap of $AUD 12.40 billion.

How does Xero make their money?

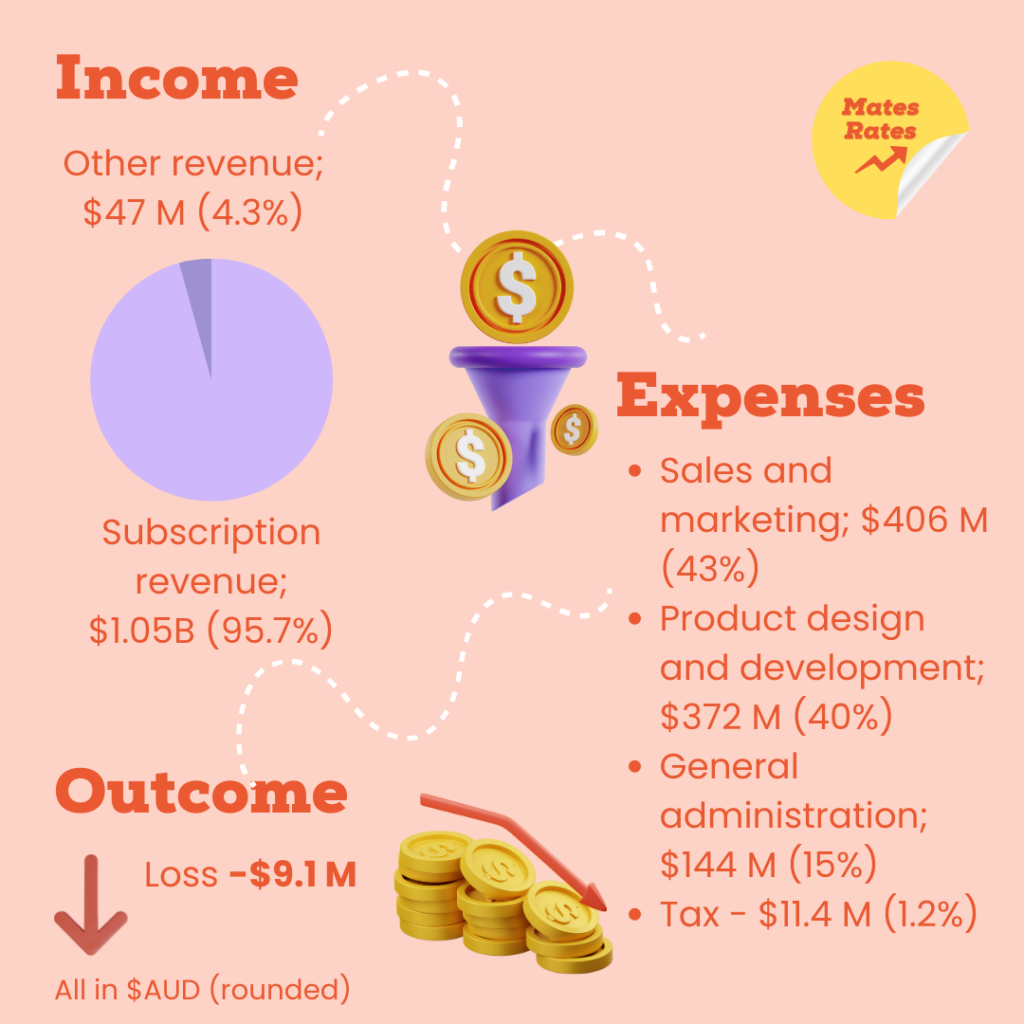

Xero generates revenue through the following segments;

- Subscription revenue

- Other operating revenue – Leveraging consumer data + Xero app store commissions.

This is highlighted in the graph below

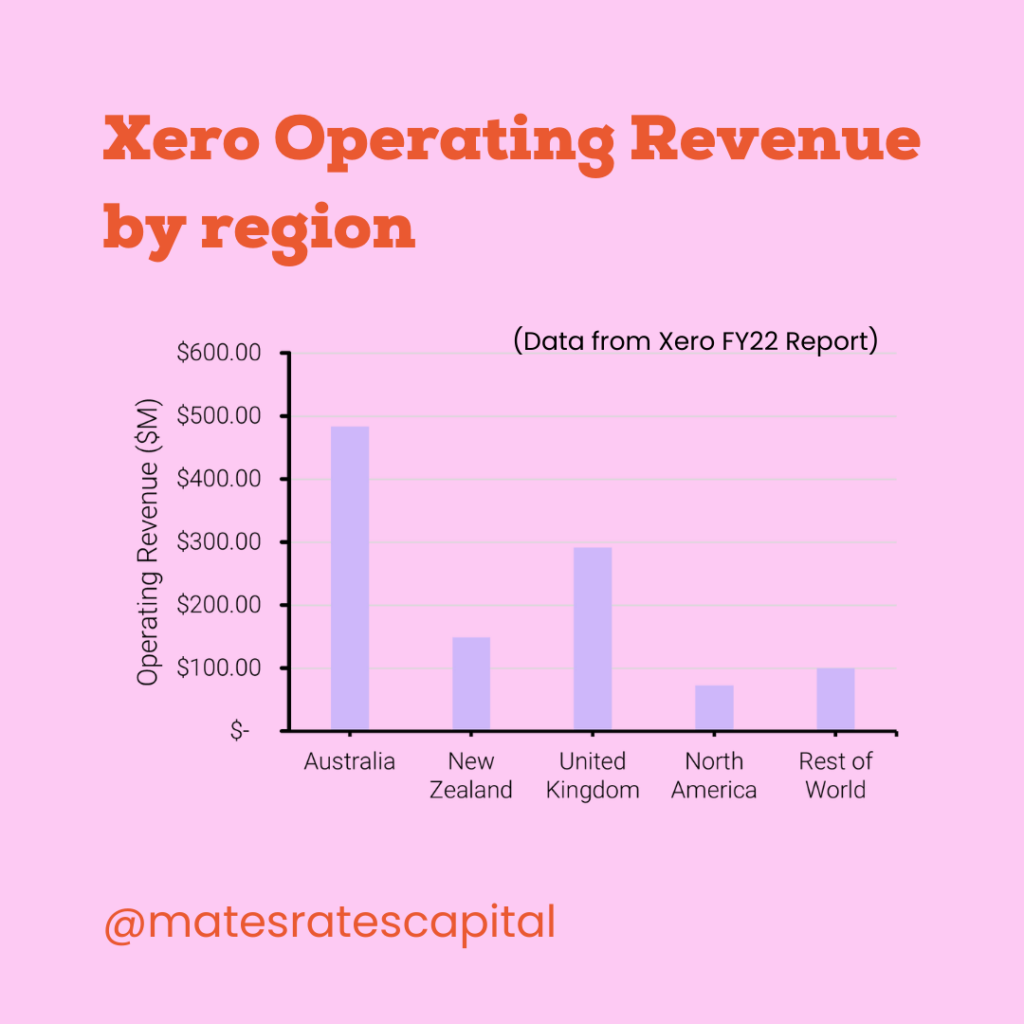

If we dive into these numbers further to get a breakdown of Xero’s revenue across different regions, we see the following:

Profitability

Xero is currently an unprofitable company, generating $1.1B in revenue yet making an overall loss of $9.1M in 2022. Furthermore, these losses are incurred despite Xero currently having solid gross margins of 87%, which means that Xero retains 87 cents for every dollar spent on producing their accounting software. With already high gross margins, there isn’t much more fat to trim in terms of reducing costs for producing Xero’s software, which is something to bear in mind when considering future profitability.

High margins are often pretty typical for SaaS companies. This is because the same code can be sold over and over again, with relatively minor cost of goods on labour for software updates and hosting fees as the company scales. In contrast, manufacturing and utility companies tend to have much lower gross margins because producing their products typically incurs high material costs.

So if Xero’s margins are so high, why are they still an unprofitable company?

The main reason is that gross margins only take into account the costs directly tied to production (i.e. hosting fees, software developer employees, customer support employees, 3rd party software), and do not factor in administrative costs, such as accountants, legal positions, sales and marketing and so on. If we dive into Xero’s income statement, we can see that almost half of their costs are dedicated to sales and marketing, amounting to $405.6M, which takes a big chunk out of their income statement.

Whether such a large spend on sales and marketing is justified, it’s hard to say. But one thing is for sure, Xero is in a highly competitive accounting software space, so it’s understandable that they’ll be splashing a lot of cash on promoting their products and protecting their brand.

Financial health

When looking at Xero’s decline in free cash over the last few years, we’re definitely planning to tread carefully. Between 2021 and 2022, Xero’s free cash flows decreased by 96% from $54.9M to $2.1M. Considering this $2.1M of free cash as a proportion of Xero’s overall revenue of $1.1B, it can be determined that less than 0.2% of Xero’s revenue – or 2 cents for every dollar earned – is available as free cash that could be used for investing in the business or building their rainy day fund.

On top of this, between 2021 and 2022, Xero’s cash and cash equivalents reduced by 61% from $658M to $404M. This primarily results from acquisition costs incurred by Xero in growing their business and product offerings, including Planday ($128.3M); a leading workforce management platform, and TaxCycle ($44.1M); a Canadian tax preparation software company. These acquisitions have lead to increased labour costs for Xero, which has played a large role in the previously mentioned drastic reduction in their free cash flows.

To put things into perspective, Xero’s current cash and cash equivalents is barely enough to cover their $405.6M sales and marketing spend, let alone all the other costs for developing products and running their business. This being said, Xero have an additional $700M available from other current assets they can tap into for liquidity, amounting to $1.1B in total current assets, which should be enough to cover a year of expenses that arise from running the business.

It also pays to be mindful that Xero are currently carrying quite a high amount of debt, with 114.8% debt relative to their equity. Fortunately, a large amount of this debt is from a $700M zero coupon loan, which is a type of debt instrument that Xero do not need to pay interest on, helping them to free up more cash flow in during tightening economic conditions – but, this comes with a catch, in that Xero have the option to offer shares to purchasers of the coupon in place of cash, which risks diluting available shares and may potentially impact the share price.

What risks does Xero face?

From our perspective, competition is by far the greatest risk that Xero faces as they work towards profitability.

Competition

Xero faces significant competition from other big players in the accounting software market, including Intuit and MYOB, who have market caps of x and x, respectively. These larger companies have more money behind them to withstand economic headwinds, plus they can potentially afford to burn cash for longer as they seek to secure new customers and seize market share.

This being said, Xero has a relatively loyal customer base that has been consistently growing over time. Despite raising the pricing of some of their subscription offerings by almost 40% over the past couple of years, in 2022 Xero saw a low churn rate of 0.90%, while increasing their number of subscribers by 19%.

Valuation

Considering that Xero is currently an unprofitable company, we will use price to sales (P:S) instead of the price to earnings (P:E) ratio to get a gauge on how the market values Xero shares. With a P:S ratio of 10.8, Xero is actually valued lower than a number of other similar listed technology companies such as Wisetech Global (P:S; 32x) and Altium (P:S; 16.5x).

Things to watch moving forward:

- Competitiveness. Constantly analysing the revenues of all of Xero’s competitors would be a massive task – and we really just cant be bothered with that. Fortunately, we can get a feel for how Xero is doing in different markets based on revenue and earnings growth in each region. Ideally, we want to see continued revenue and earnings growth, particularly in international segments, such as US and Canada, which are markets where Xero has made a number of acquisitions, including Planday and TaxCycle.

- Cash flow. In 2022, Xero saw a depletion of free cash flow by 96%, primarily due to increased labour costs arising from the acquisition of Planday and TaxCycle. While Xero should have enough liquidity from current assets to last them a year, their current cashflow situation simply isn’t sustainable, so we’ll be wanting to see a return on these acquisitions through an increase in cash flow.

When focusing on Xero’s annual losses, reductions in cash, and risk of competition, it may feel like we’ve painted a pretty gloomy picture. However, that’s not to say there isn’t room for growth. Overall, the US presents are large available target market for new subscribers, which may be just what Xero need to reach profitability.